Following its February 3 +25 rate hike, pushed by rising inflation concerns, the Reserve Bank of Australia raised them another +25 bps today.

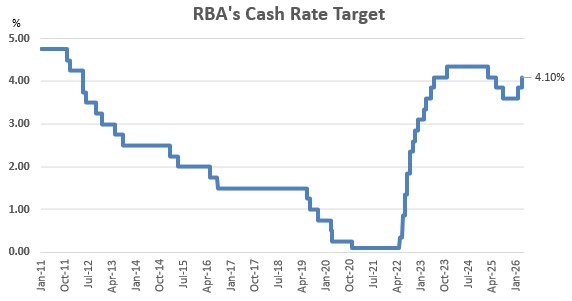

That takes their cash rate target up to 4.1%.

It was last at this level in Mar 2025, on its way down from the recent high of 4.35% that lasted 16 months from November 2023 until February 2025.

The reversal has all the hallmarks of looking like the February 2025 cutting cycle has been a mistake (with the benefits of hindsight).

Today's rise comes with a deteriorating inflation situation, one the RBA will find it hard to confront because it is essentially a supply shock we are getting from Trump's war, rather than the demand issues that caused it to act in February. Really, it is the confluence of both that is worrying, with CPI inflation running at 3.8% in January and unlikely to be less in February.

Banks have been raising their savings and term deposit rates in anticipation, as well as raising fixed home loan rates. Today's hike gives the green light to a comprehensive round of matching variable rate hikes.

You can keep up to date with all the rate changes by banks here for home loans, here for savings accounts, and here and here for term deposits.

Higher rates may well take the sting out of the fast-rising housing markets, and that is probably the RBA's intent even though their talk is all about inflation. Rising house prices feed into inflation expectations in a significant way. And these expectations weigh heavily on policymakers when they look at trying to keep inflation close to the mid-point of their 1-3% band.

Just after the decision, the ASX200 rose, now recording a gain of +0.2%. The AUD eased very slightly to 70.6 USc. The AGB 10yr yield slipped slightly to 4.925%.

Here is the Statement by Governor Bullock on today's move.

At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 4.10 per cent.

While inflation has fallen substantially since its peak in 2022, it picked up materially in the second half of 2025. Information since the February meeting suggests that some of the increase in inflation reflects greater capacity pressures. In addition, the conflict in the Middle East has resulted in sharply higher fuel prices, which, if sustained, will add to inflation. Short-term measures of inflation expectations have already risen. As a result, the Board judged that there is a material risk that inflation will remain above target for longer than previously anticipated.

Higher capacity pressures reflect, in part, the greater momentum in demand in the latter part of 2025. Growth in private demand strengthened substantially more than was expected in mid-2025, although the composition of that growth surprised in the December quarter. Business investment was above expectations and consumption was below expectations. Meanwhile, growth in unit labour costs declined. More recently, the unemployment rate has been a little lower than expected and measures of labour underutilisation remain at low rates. Activity and prices in the housing market grew strongly over the past year, although housing price growth moderated somewhat at the start of 2026.

Financial conditions have tightened a little this year, but the extent to which monetary policy is restrictive is uncertain. Credit is readily available to both households and businesses and the effects of interest rate reductions in 2025 are yet to flow through fully to aggregate demand, prices and wages. The exchange rate, money market interest rates and government bond yields have risen over the past month. In large part, higher interest rates reflect expectations for the path of monetary policy, which have risen in Australia and most other advanced economies in response to the expected inflationary implications of the conflict in the Middle East.

There are material uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy is restrictive. Globally, the conflict in the Middle East poses substantial risks in both directions. A longer or more severe conflict could put further upward pressure on global energy prices; this will push up near-term inflation and could also increase inflation further out if it impairs supply capacity or price rises get built into longer term inflation expectations. Higher prices and prolonged uncertainty may cause growth to be lower in Australia’s major trading partners and also in Australia.

Decision

A wide range of data over recent months have confirmed that inflationary pressures picked up materially in the second half of 2025. While part of the pick-up in inflation is assessed to reflect temporary factors, the Board judged that the labour market has tightened a little recently and capacity pressures are slightly greater than previously assessed. Developments in the Middle East remain highly uncertain, but under a wide range of possible scenarios could add to global and domestic inflation.

In light of these considerations, the Board judged that inflation is likely to remain above target for some time and that the risks have tilted further to the upside, including to inflation expectations. It was therefore appropriate to increase the cash rate target.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand and the outlook for inflation and the labour market. Monetary policy is well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment. It will do what it considers necessary to achieve that outcome.

Today’s policy decision was made by majority: five members voted to increase the cash rate target by 25 basis points to 4.10 per cent; four members voted to leave the cash rate target unchanged at 3.85 per cent.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.