We have noted the strength of Macquarie's growing position in household deposits, but they have equal growth strengths in home loans as well.

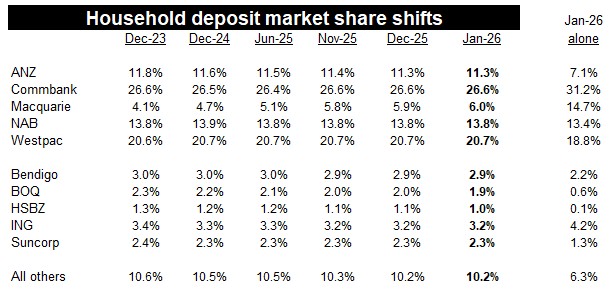

Here is how their market shares are shifting in household deposits.

'Everyone' is either losing share, or holding - except Macquarie who is making major advances. If we isolate on the January share, perhaps you can say Commbank and ING are making some recent progress, but it is minor compared to the outsized growth by Macbank.

This is why we are seeing the advent of 5% and higher term deposit rates. We have noted Bank Australia, Great Southern Bank, and Qudos earlier in the week with their 5%+ rates.

Now we can report that AMP has also hiked, and significantly. with 5% rates for terms of either ten or eleven months, and 5.15% for a one year term.

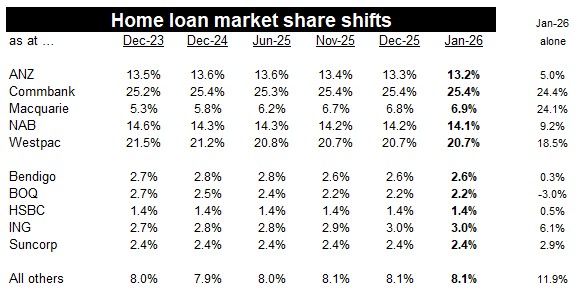

And here is how market shares are shifting in home loans (both owner-occupied and investors lending). It's a similar story.

Here ING is the only other one gaining market share in a notable way. But nothing like what Macbank is achieving.

Today, (Friday, March 20) Macbank has raised all its fixed rates by +25 bps. They have been joined by Bank of Queensland and AMP.

Clearly, consumers are winning better deals from all this competition. This is what competition is supposed to do for them.

But while we are at it, we do need to note that the big four-pillar banks operate with a regulatory handbrake. They have broad social requirements to make comprehensive offers which can include many options for specific customer groups that aren't very profitable. And they are essentially required to maintain a comprehensive branch network offering full legacy services, especially in regional Australia. None of these requirements apply to Macquarie. They have offers only in the most profitable section of the market, and no extensive branch network, certainly not in regional Australia. The lack of these limits gives them very significant competitive advantages.

If Macbank maintained their current growth in household deposits, they could rival ANZ with just a few year. In home loans it will take them much longer, but they are on their way.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.