Providing funding for borrowers to buy a house is now a $2.475 tln honeypot.

And it is one that grew +7.0% in the year to April 2026, according to the latest APRA data. That is the fastest growth rate since the pandemic splurge between October 2021 and September 2022.

But some banks are harvesting this 'gold' much better than others.

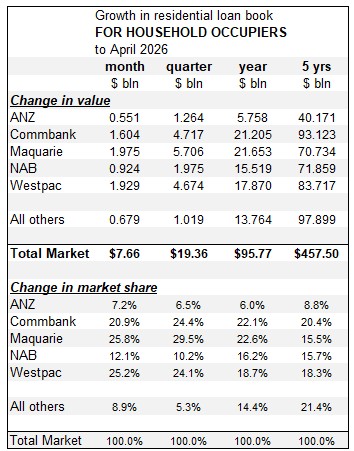

The recent stand-out performer is Macquarie Bank. They now have a 7.2% overall market share but they are won 24.6% of the new business in April 2026. That is better than market behemoth Commbank, who won 'only' 21.3% in April.

But Macquarie wasn't the only winner. In fact Westpac won 23.7% in a comeback performance.

But the best way to look at the winners & losers in the national mortgage market, is to look at it in its two major components: lending to household occupiers, separate to lending to household property investors.

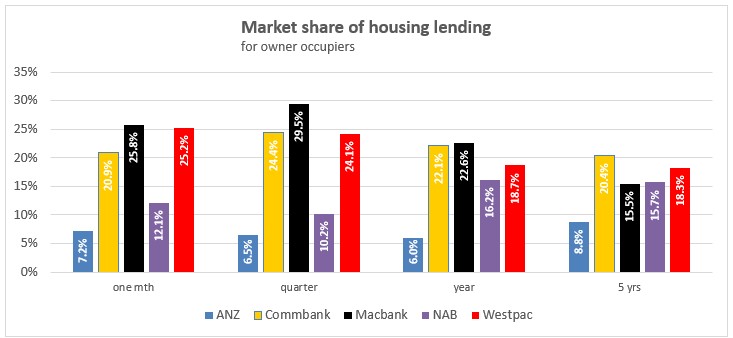

Household occupiers

While Macquarie is clearly winning outsized market share and with the headline performance, Westpac is showing renewed competitiveness. Commbank is holding on, but only just. ANZ and NAB are the two laggards.

Looking a bit wider, to encompass the many challenger banks to these big five, we can see them losing their long term market share of about 22%, and it had been falling away rather quickly even if it did recover somewhat in April to almost 9%

ANZ is not strong in lending to households to buy their own home. But for all the others, this has been their primary focus

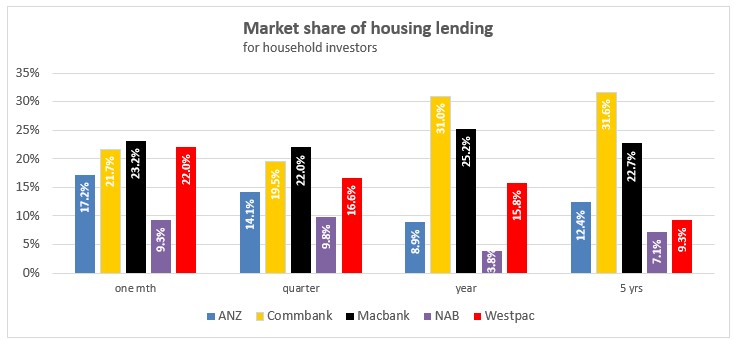

Household investors in residential housing

ANZ is stronger in lending to households who invest in residential property. And over the past quarter and past year, ANZ has clearly made headway in this sector.

Again the winner through is Macbank, now matched by Westpac, with Commbank struggling to retain its historic market dominance.

NAB is the also-ran in this sector.

Looking wider, it is also clear than the challenger banks are after-thoughts when it comes to investing in residential property.

If you are buying to occupy, the cost of a mortgage is just one part (even if it is important) of how you secure your residence. In addition, there is a lot of emotional capital tied up in "your home".

But if you are an investor, what you own is not "a home"; it is just a financial investment. To ensure it returns a yield commensurate with the risks involved requires you to look at the numbers with a business eye. Getting the best mortgage deal is important and changing lanes when the facts (i.e. interest rates) change is a smart thing to do.

Our home loan interest rate tables can be set for investor loans, variable or fixed, P&I or interest-only.

All the data in this analysis is from the APRA monthly releases.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.