by Justin Smirk*

As noted in our Middle East Crisis Update, a prolonged disruption in the Gulf is sustaining higher energy prices. We now have Brent averaging around US$120/bbl in the June quarter. This is based on our assessment of unfolding infrastructure damage and a slow recovery in shipping traffic through the Strait of Hormuz.

So despite the announced cut in fuel excise, we expect CPI inflation to peak at 5.4%yr in the June quarter, while the monthly measure, which the ABS highlights as the main indicator and can be significantly more volatile that the quarterly series, may peak close to 6%yr in May.

Westpac expects core inflation, as measured by the quarterly Trimmed Mean, peaking around 4% in the second half of year; food, household services and even new dwelling prices, alongside broader non‑energy pass‑through, are key risks to our estimates. We also note that the monthly TM spikes a bit faster hitting a 4.0%yr pace by June.

In response, the RBA is now expected to deliver three rate hikes (May, June, August), taking the cash rate to a peak of 4.85%. As the combined supply shock and tighter policy weigh on demand, GDP growth is expected to trough at 1%yr in 2027 while unemployment peaks around 5% at end 2026. A deeper dive into these issue are summarised in the video by the Westpac Economics Team led by Luci Ellis “Longer conflict, higher inflation and cash rate”

This was, of course, before the announcement of a two-week ceasefire on the 8th of April (Asian time). This is obviously welcome and a positive risk scenario relative to the baseline we outlined last week and underpins our current inflation forecasts. Should the ceasefire hold – and that is a big if – a faster opening up of the Strait of Hormuz would result in energy prices tracking between the profile we currently have and the one underpinning the forecasts in the March Market Outlook (which was based on a one-month closure of the Strait with little infrastructure damage). For further background on the unfolding risks to our current scenario see Luci Ellis’s note “On hoping you are wrong”.

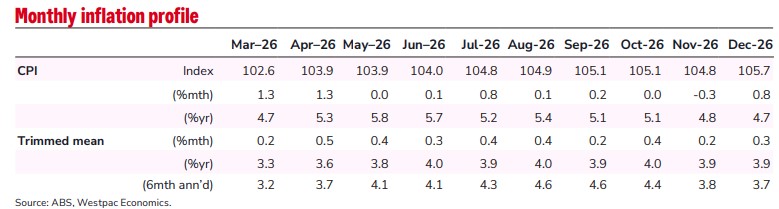

In this bulletin we are also release a forward profile of the Monthly CPI. This process is still at a preliminary stage but given the extreme surge we expect to see in the Monthly CPI, we thought it would be timely to provide some guidance out to December 2026.

March and April headline CPI set to surge

The Israel/US assault on Iran began in the morning of the 28th of February. We expect the resulting surge in oil prices to have the largest hit to the CPI in the months of March and April before flattening out in May and June. Auto fuel is set to increase again in July but this is due to the expiration of the recent temporary reduction in fuel excise.

Westpac is forecasting a 1.3% increase in March on the back of a 35% increase in auto fuel. At two decimal points the increase is 1.26% but we warn that given the current volatility in prices, there is a greater than usual degree of uncertainty so these finer estimates should be used with even more caution than usual.

The annual pace lifts from 3.7%yr to 4.7%yr in March.

Our current scenario has auto fuel lifting a further 2% and 6% respectively in April and May. The April CPI will also be boosted by a seasonal bounce in clothing & footwear and holiday travel & accommodation plus the annual increase in health insurance premiums. The annual pace of CPI inflation is expected to peak at 5.8%yr in May (so there is a risk it could peak as high as 6%yr) and then slowly moderate to 4.7%yr by December 2026.

Core inflation is higher for longer

We estimate a 0.23% mth rise in the Monthly Trimmed Mean (TM) in March holding the annual pace steady at 3.3%yr. The six‑month annualised pace is also steady at 3.3%yr which down from a 3.7%yr pace in December. We were expecting the pace of core inflation to moderate from here but with the conflict in Iran disrupting shipping out of the Gulf, and the resulting surge in fuel prices, we now see fuel prices remaining higher for longer resulting in a greater degree of pass -through to core inflation.

The TM is set to lift 0.5%mth/3.6%yr in April, 0.4%mth/3.8%yr in May and 0.3%mth/4.0%yr in June. The forecast peak in the annual TM inflation is 4.0%yr in June then holding between 3.9%yr and 4.0%yr to year end; in six -month annualised terms the peak pace is 4.6%yr in September.

Quarterly inflation less volatile

The Monthly CPI is the focus of the ABS CPI release, and as such, it gains the most media attention. However, at least for now given the short history of the complete Monthly CPI, the quarterly measures of inflation will remain the focus of both the RBA and the Australian government when setting both monetary and fiscal policy, particularly when it comes to core inflation as measured by the Trimmed Mean.

As the current conflict started in the last week of February, we have only see one month of higher fuel prices so the auto fuel is expected to rise just 5.9% in the March quarter. However, starting from a high base in the June quarter means fuel prices to continue to rise solidly and we estimate a 24% surge in the fuel prices component in the June quarter.

Overall, we estimate a 1.5% increase in the March quarter taking the annual pace from 3.6%yr to 4.7%yr. As noted earlier, we expect this momentum to continue into the June quarter with a further 1.9% surge in the CPI taking the annual pace to 5.4%yr. While we think this should be the peak in the annual pace, it is nevertheless the fastest pace since June 2023 when it was reported to be 6.0%.

Core inflation is not immune to this boost as we are forecasting a 0.93% increase in the March quarter, matching the 0.9% increase in the December quarter and it is a prelude to the step up to a 1.0% increase in both the June and September quarters. This will see the annual pace peak at 4.0%yr in the second half of the year.

The Trimmed Mean estimate starts from a low of 0.2% to a high of 2.2%. Significant expenditure items trimmed off the bottom includes vegetables (–1.2%), international travel & accommodation (–0.7%) and other non -durable household products (–0.7%). Trimmed off the top are secondary education (2.3%), tobacco (2.4%), furniture (3.3%), women’s garments (3.5%), auto fuel (5.9%), electricity (118.3%).

As we have noted in earlier bulletins, until the ABS has a better understanding of the seasonality of the new monthly CPI, they will continue publishing quarterly underlying inflation measures in a manner consistent with the history of price collection frequency. We have replicated this process and found it represents a small downside risk to our March quarter estimate but it still rounds to 0.9%qtr. As such we just note the risk and do not adjust our overall forecast.

Signs of faster pass-through

We have received many anecdotal reports of increases in input costs, often as a fuel surcharge or levy. Some of these were adjusted downwards when the Australian government cut the fuel excise but remain significant. We have also heard of restaurants, cafés and even hairdressers adding a fuel levy to prices but these are yet to be confirmed.

It has also been reported that rising input costs could add as much as 10%, or $50,000, to the cost of building an average detached home. Using input price increases as reported by Tradelink this estimate seems fair. Tradelink data suggests an average increase of 16% in April, the largest increase in the data we have back to January 2020; not all products will see price increases in any given month, but the number of notifications of price increases on the Tradeline website has also risen. The proposed average increase for May increases to 17% before easing back to around 7% in June and July so it will be interesting to see how these estimates are adjusted as actual prices are posted.

Justin Smirk is a Senior Economist at Westpac. This is a re-post from the original here.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.