The Federal Government Budget was released last night, and all the major documents are available here and here.

But for most of us, that is detail we fund hard to absorb and comprehend.

So here is one professional analyst's non-partisan review.

By Pat Bustamante, a senior economist at Westpac

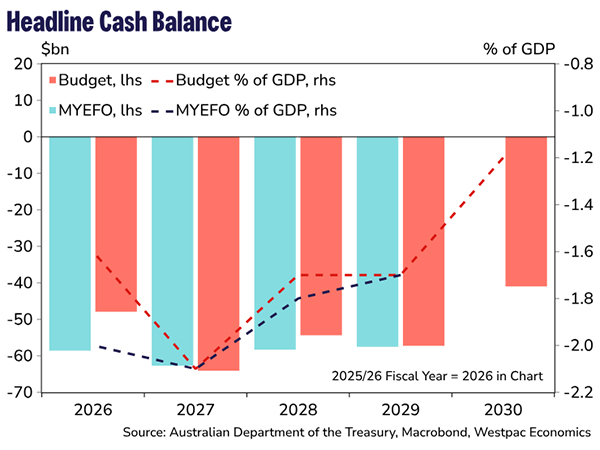

The underlying cash deficit is expected to be $28.3bn in FY2026 (improvement of around $8.5bn compared with the December MYEFO), increasing to $34.4bn in FY2029, before improving to $25.3bn in FY2030 when the tax measures and NDIS saves start to mature.

Compared with the December 2025/26 MYEFO, there was an improvement of around $45bn across the five years to FY2030. As we expected, positive economic variations, due to the stronger economy and higher than expected commodity prices, delivered a net windfall of $36.6bn over the forwards. In addition, policy decisions taken by the Government delivered a net save to the bottom line of around $8.2bn over the forwards

The fiscal impulse remains slightly expansionary

Savings from the policy decisions are back‑loaded. In fact, over the first three years of the forward estimates period (to FY2028) discretionary measures add to the fiscal impulse, which remains slightly expansionary. The headline deficit, which also includes “off budget spending”, increases from a deficit of 0.8% of GDP in FY2025 to 1.6% in FY2026 and 2.1% in FY2027.

In addition, the payments to GDP ratio is expected to remain elevated rising from 26.2% of GDP in FY2025 to 26.2% of GDP in FY2026 and 26.8% in FY2027 and FY2028 – outside of the pandemic, it is still the highest share of GDP since FY1987.

A tale of two horizons

The savings package (mainly tax and NDIS) is one on the largest in the past 30–35 years, dating back to the mid‑1990s. It is significant both in nominal terms and as a share of GDP.

But the saves are largely backloaded and ramp up over the medium term. In total, by FY2037 these saves improve the bottom line by 1.0% of GDP (and 1.3% of GDP when you include the public debt interest impacts) from 0.1% of GDP in the budget year (FY2027) and 0.5% of GDP in the final year of the forwards FY2030.

On taxes, the leaked changes to negative gearing and the capital gains discount were confirmed. The minor surprise was a “loss carry forward” for losses on rental property that from 1 July 2027 will be no longer be available for investors to offset taxes on other sources of income. Grandfathering will apply to existing negatively geared properties, with investors in new dwellings exempt from the changes and still able to access the 50% CGT discount going forward.

The 30% minimum tax on trusts distributions was also confirmed, raising around $4.4bn at maturity in FY2030. In addition, the government will extend venture capital concessions, provide access to the loss carry-back mechanism for SMEs, enable small start-ups to claim a refund on tax losses over the first two years of their lives and implement the Working Australian Tax Offset on a permanent basis. In net terms, these changes to taxes will generate a net improvement of around $80bn over the next decade and about 0.3% of GDP at maturity (in FY2037). NDIS saves also ramp up over the medium term, increasing to around 0.7% of GDP.

A surprising absence and some positive steps

Typically, when governments broaden the tax base (i.e. remove access to, or reduce, concessions like the CGT 50% discount), they do so to lower the tax rates. That didn’t occur and perhaps that will come down the track, perhaps in the lead-in to the 2028 election. Workers receiving an immediate downpayment through the ongoing workers offset (which reduces taxes by around $3.3bn a year).

Other notable packages include the productivity and economic resilience package.

The productivity package is a step in the right direction and if fully implemented has the potential to move the dial on productivity growth. Building a single national market with a national licensing system and by harmonising payroll tax administration will help labour and capital flow to where its mostly needed, boosting efficiency.

Speeding up approvals will reduce the risk of projects being shelved while the changes to tax arrangements for small businesses and startups can encourage risk taking. In addition, getting rid of charges for licensing standards and making it quicker for migrants to use their trade skills will also help boost productivity.

Economic resilience will also be helped from the $15bn fuel package with the Government setting up the $7.5bn fuel and fertiliser security facility and announcing the $3.2bn Government operated fuel reserve. This is in addition to the $1bn of concessional loans for businesses impacted by the fuel shock. Making electric vehicle tax concessions permanent to encourage take-up and reduce reliance on fuel will also help boost resilience.

Bottom line

Despite the lack of surprises on the night, this will be a budget to remember. The changes to housing taxation are generational and will shape the system for years to come. The productivity package is also significant, particularly in areas where there is harmonisation across the federation.

In the short term, the budget will be slightly expansionary and walking a fine line in an environment of inflation pressures. Given that the savings measures ramp up over time, follow-though and full implementation will be important. That is unlikely to be straightforward. The Greens have already signalled they will not support key elements of the NDIS changes, while the Coalition has previously indicated it will oppose reforms to housing taxation and discretionary trusts.

Further detail are available in our full report here.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.