If you are on a variable home loan variable, you can lock in a similar rate now by moving to a one year fixed rate and avoid the next upcoming RBA rate hike.

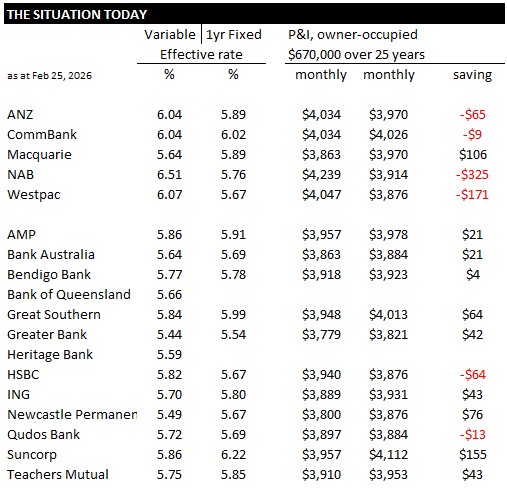

You can use our smart home loan rate table to find the effective rate for your individual situation.

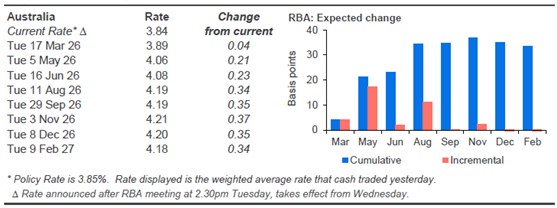

Financial markets - and just about every professional analyst - thinks that the RBA will raise rates again on May 5, 2026 by another +25 bps. That would take the cash rate target to 4.1%.

But we should point out, this isn't a certainty.

It is likely however.

If you accept that, shifting from a floating rate now to a one year fixed rate could save you real money if you bank at most of the main banks. Only at Macquarie would you be better off by staying with a variable rate at this time. At NAB and Westpac the monthly savings exceed $100 per month, even now.

If the May 17, 2026 RBA rate hike happens as expected, those savings will swell everywhere.

By that time, it is reasonable to think that fixed rated will have risen. So that is why moving early could pay off handsomely. But you need to get in before financial markets price the one year fixed rate higher and the banks move those fixed rates up.

The examples above are representative only. They apply for an owner-occupier loan over 25 years with a 60% plus LVR for a $670,000 loan size (the average, per APRA stats) on a P&I basis. Other assumptions will give different results. Get professional advice before you make any commitment.

Our mortgage rate table allows you to reset the parameters to fit your specific situation.

But fixing now before the expected May 17 RBA rate hike could be a smart financial decision no matter who you have your home loan with.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.