Content sourced from the Word Gold Council. The original is here.

Australia’s economy continues to grow but resurgent inflation and the Reserve Bank of Australia (RBA)’s decision to resume tightening in February 2026 – diverging from some of its peers – raises questions around portfolio allocations. Australia's unique geopolitical positioning, with its fortunes tied to increasingly affluent trade partners within the Indo-Pacific while being strategically aligned with the US, has created an asymmetry that makes portfolio diversification crucial.

Against this backdrop, gold’s role in Australian portfolios warrants renewed attention. This report finds that gold has delivered positive returns across all RBA rate regimes since 2010, appreciated notably in AUD terms since 2022, and provides meaningful downside protection during equity stress. For Australian investors, a strategic allocation to gold offers both a macro hedge and a portfolio diversifier at a time when uncertainty takes centre stage.

The 2026 macro picture

Economic resilience and inflation pressure

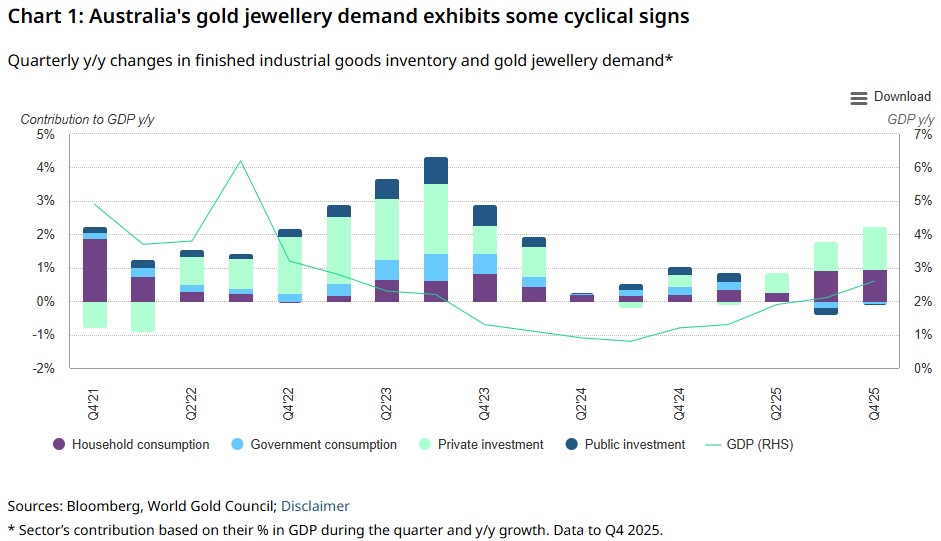

Australia’s economy has extended its growth streak through 17 consecutive quarters in Q4 2025 with GDP expanding 2.6% y/y. This comes on the back of private investments (Chart 1) – which grew at their strongest pace since Q4 2021, led by growth in dwelling construction and in data centres in New South Wales and Victoria.1

However, this growth has been accompanied by resurgent inflationary pressures. Strong private sector demand and labour market tightness, with unemployment hovering around 4.2%, continue to generate wage pressures that may feed through to consumer prices. Meanwhile, electricity costs have also surged since mid-2023 as Australia navigates the energy transition from coal to renewables, further adding to structural inflationary pressures.

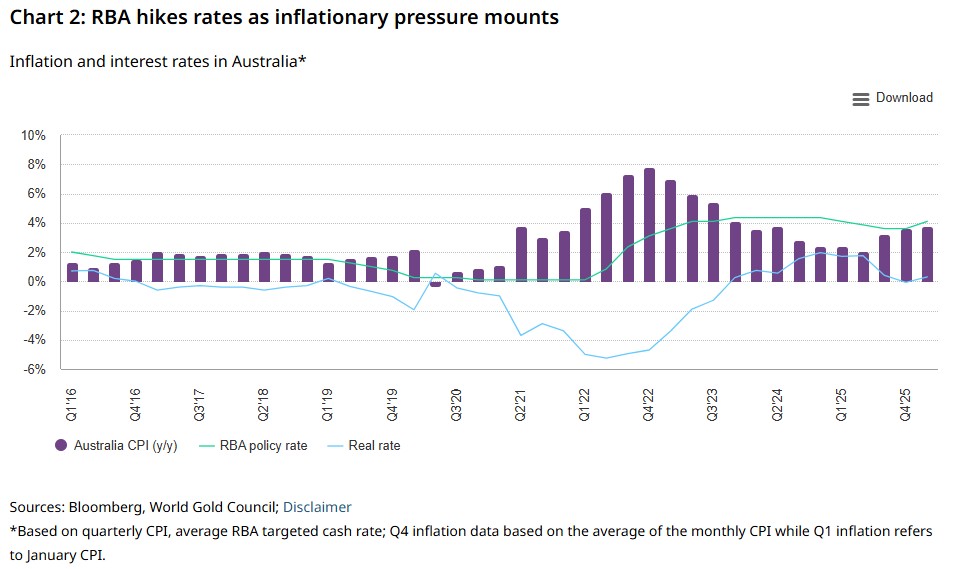

These challenges have shifted the RBA from a cautious hold to active tightening. Australian CPI rebounded to 3.8% in January 2026, and the RBA raised the cash rate by 25 basis points to 3.85% in February – the first hike since November 2023 (Chart 2). The recent war in the Middle East sparked further inflationary concerns, prompting the RBA to hike rates again in March to 4.1% citing geopolitical risks and the resultant inflationary pressure as key reasons.2

Trade uncertainties loom

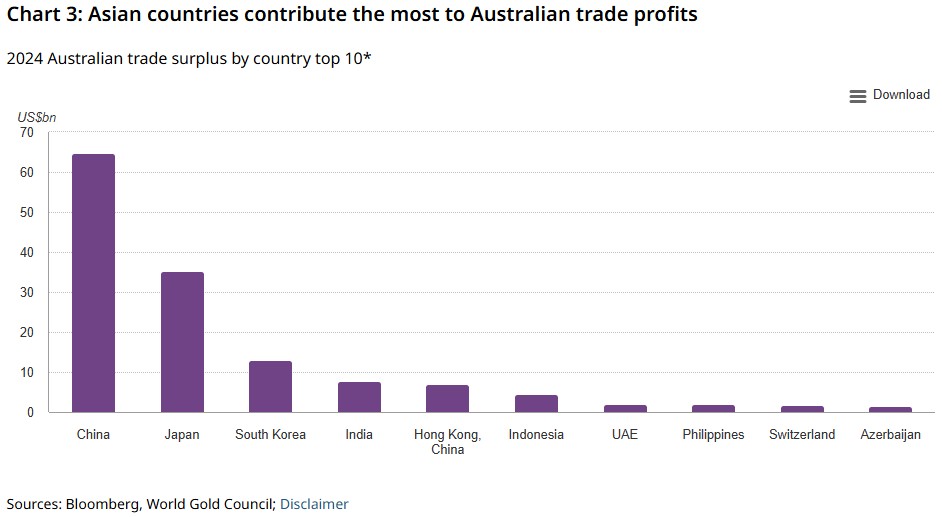

Australia’s geopolitical position with the West and its trade reliance on Asian countries mean it is vulnerable of both geopolitical shocks and economic uncertainties. Australia’s political stance aligns with Western countries. Yet Asian countries such as China, Japan, South Korea and India, contributes the most to Australian trade surplus (Chart 3). This puts the country between a rock and a hard place, especially if tensions between the East and the West rises. Such uncertainties could lead to negative impacts on its economy.

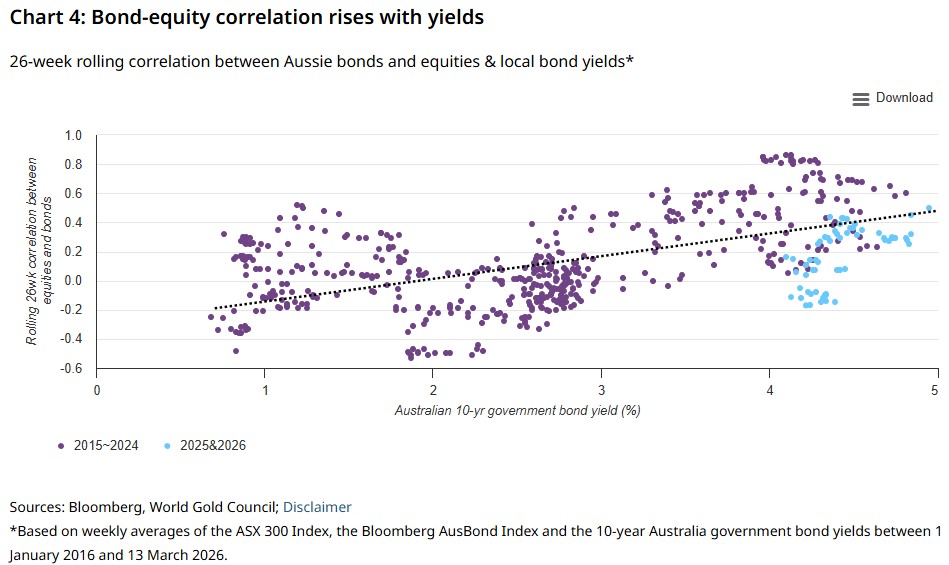

What do these mean for Australian investors? First, local investors should re-think the relationship between bonds and equities. Inflationary concerns are likely to keep the RBA on a hawkish bias in future rate decisions. Both rising inflation potential and possible further rate hikes are likely to push up local yields, weighing on bonds. And our analysis shows that the correlation between bonds and equities rises alongside bond yields (Chart 4)– as inflation and higher rates adversely affects both assets.

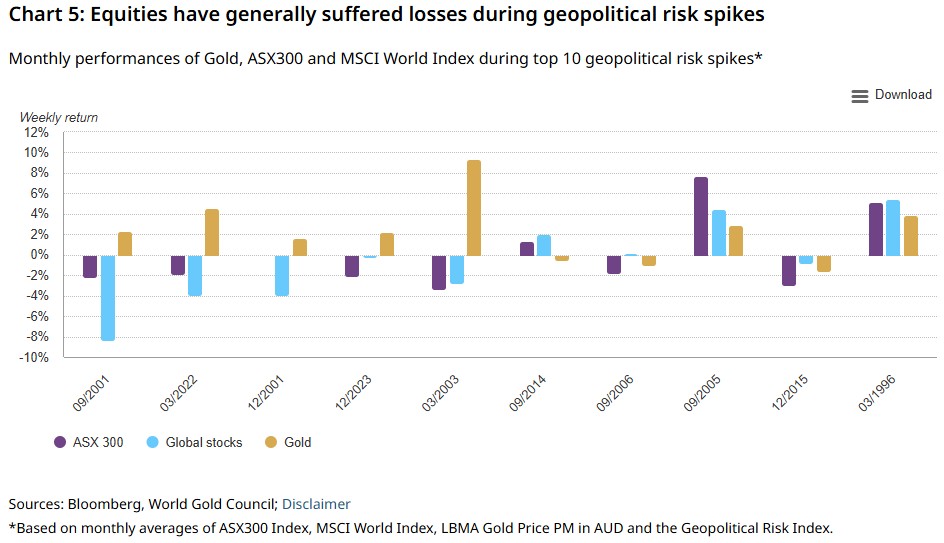

Meanwhile, renewed spikes in geopolitical risk could pose headwinds for the Australian economy, given its heavy reliance on exports. Historical patterns suggest that geopolitical risk shocks tend to cluster, and during most such episodes, both domestic and global equities have come under pressure (Chart 5).

Gold’s strategic place in Australian portfolios

Gold, the asset independent from Australian’s macro drivers

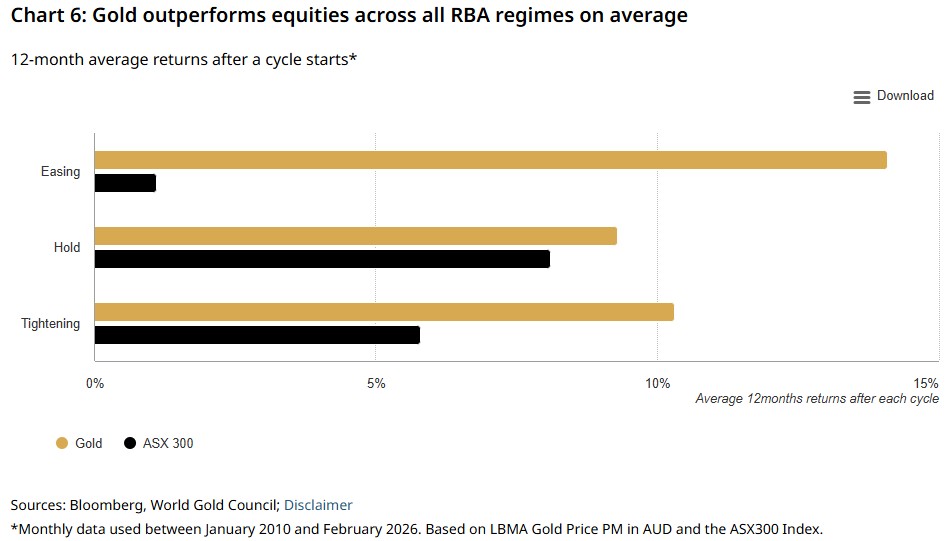

Investors consider opportunity costs when allocating into any asset class, and with the RBA back in tightening mode, a natural question arises: do Australian rate cycles meaningfully impact gold returns? As it turns out, not much.

Gold has historically delivered positive returns across tightening, hold and easing environments, with no clear evidence that rising rates impair gold performance, when priced in AUD. Moreover, gold delivered a higher average 12-month forward return than Australian equities in every RBA regime. The gap is most pronounced during easing cycles, when gold returned 14% - partially fuelled by potential AUD depreciation during such mode – and equities returned around 1% on average (Chart 6).

This is mainly because gold is driven by supply and demand dynamics determined globally. For instance, global geopolitical risks, inflation and major central banks’ monetary policy paths collectively impact investment demand for gold from investors worldwide – including those from Australia. This underscores gold’s role as a global asset that is largely independent of Australia’s domestic monetary cycle.

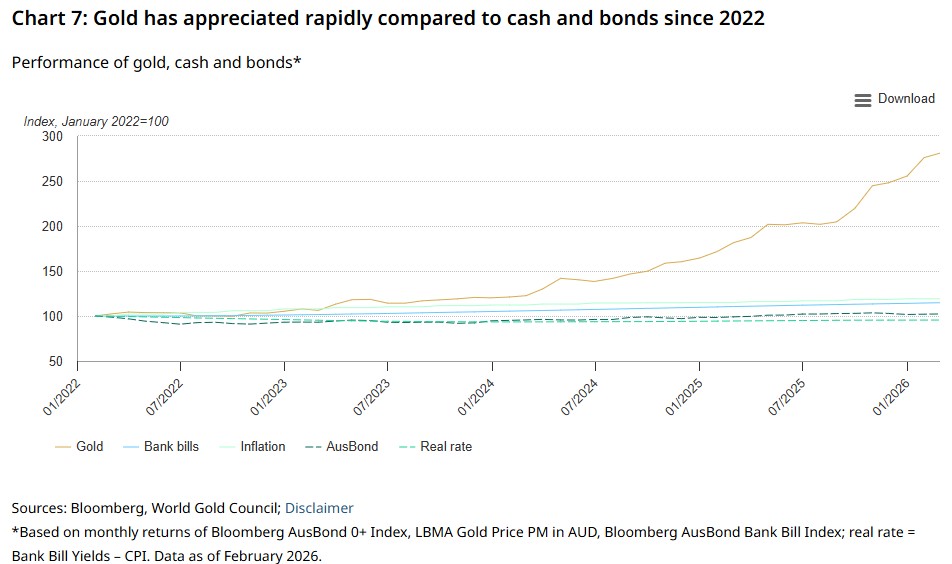

In fact, the past four years provides a meaningful stress test. RBA started tightening in 2022, making cash deposits attractive after ultra-low rates. Between 2022 and now, gold appreciated by approximately 181%, which more than offset the opportunity cost of holding a non-yielding asset. During this period, fixed income investors saw real returns fall around to 95 cents to the dollar with nominal returns rising by around 2% (Chart 7).

An effective portfolio risk diversifier

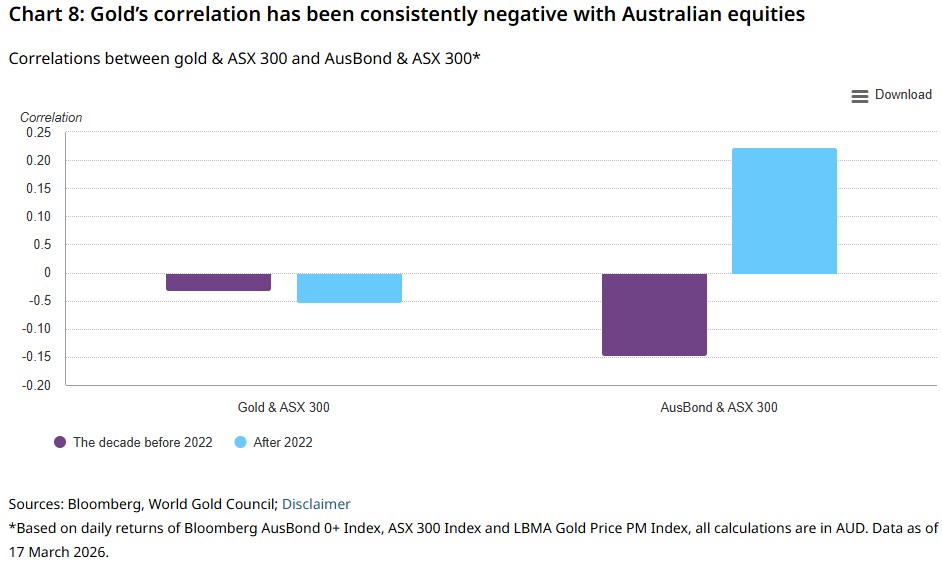

As correlations between local bonds and equities continue to rise, investors’ search for effective diversifiers has intensified. Since 2022, structurally higher global inflation and more frequent geopolitical shocks have driven bond–equity correlations higher, as discussed earlier. Yet gold has maintained a consistently negative relationship with Australian equities over time, offering investors a reliable source of diversification and portfolio resilience (Chart 8).

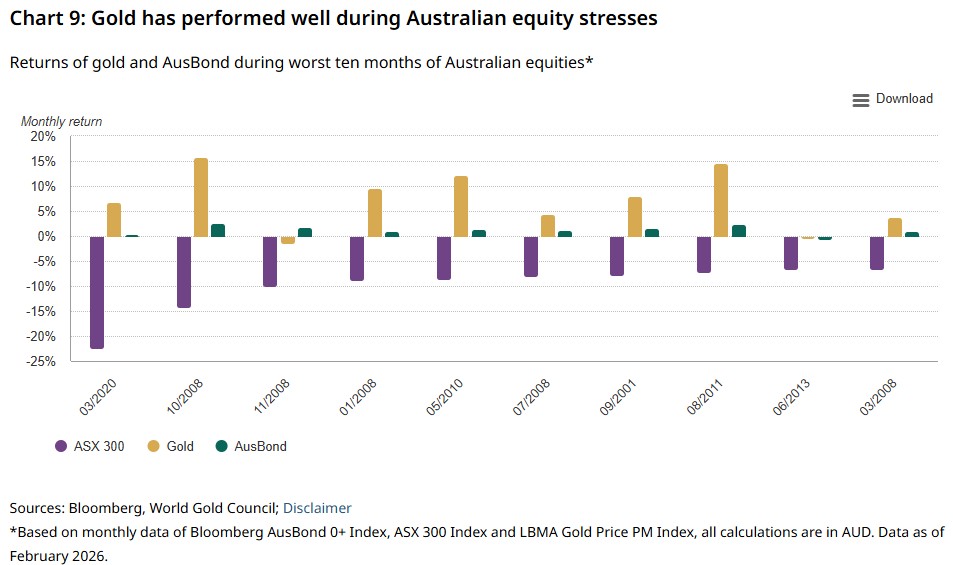

Indeed, gold has been put to the test during periods of systemic market stress and over the years has proven to be the asset class that performed better than others during such periods (Chart 9). And gold has also generally cushioned portfolio losses when geopolitical risks spike (Chart 5) – with the most recent case in point being the US-Israel-Iran conflict where gold rose on the first trading day after the war.

Key takeaways

Gold's performance is driven by a diverse set of global factors that operate largely independently of domestic interest rate policy. The question for Australian investors is no longer whether gold belongs in portfolios, but how can it not.

Gold performs well across all interest rate market regimes. Since 2010, gold has delivered positive 12-month forward returns whether the RBA was tightening, holding or easing, with no clear evidence that rising rates impair performance in AUD terms.

The case for diversification has only grown stronger. Geopolitical uncertainty, while episodic, keeps the diversification argument for gold intact as each new shock tests a portfolio’s ability to sustain through the episode.

The opportunity cost argument. This often works against gold, but since 2022, gold appreciated notably in AUD terms while cash deposits yielded around 3% and fixed income instruments saw real returns fall.

In summary, we believe gold’s role as a strategic asset for Australian investors remains highly relevant, more so now than ever.

Footnotes

2. See: Statement by the Monetary Policy Board: Monetary Policy Decision | Media Releases | RBA

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.