This is not analysis for home owners who have trouble looking ahead.

But if you can, this is what you face.

Let's assume you have a home loan on a variable rate.

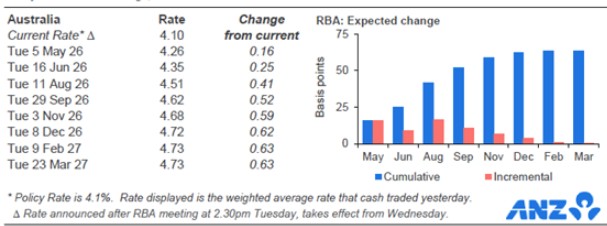

Financial markets have priced in two full +25 bps rate hikes in 2026 from here.

This is entirely based on what they think the RBA will do in response to rising inflation pressures. And it is supported by comments made directly by RBA governor Bullock.

Rate hikes are coming. And they will be matched directly by hikes in bank variable home loan rates.

Wait, you say - fixed rates have been rising recently too, and those increases happen more frequently than the variable rate roses triggered by the RBA.

True, but fixed rates are 'fixed' for the period to take them out for.

In a rising market, you can assess the fixed rate benefits.

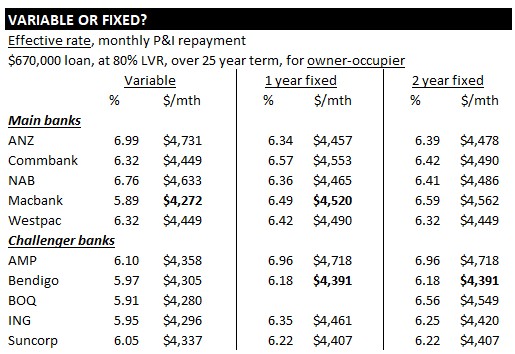

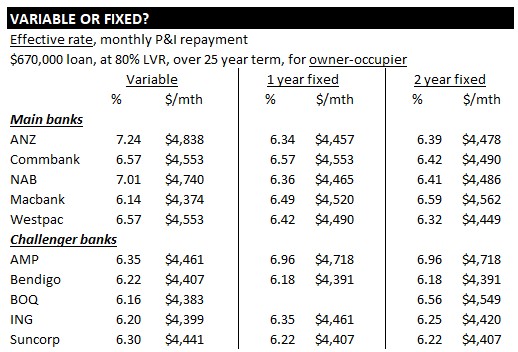

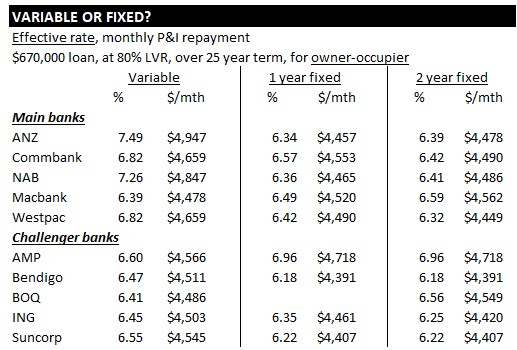

Here is where they are (on an 'effective rate' basis):

If you switched to a one year fixed rate now, you will avoid all the interim variable rate hikes, and lock in some certainty on your repayments.

If you switched to a two year fixed rate now, that 'certainty' would last twice as long - but you might miss out to some posential 2027 or 2028 rate decreases. But you have to believe that the current inflation pressures are transitory, and that the RBA policy moves to get inflation under control. However, the bald fact is, the RBA has always been too slow to act or react to inflation pressures.

After the June 15 +25 bps RBA rate hike, if you switch to a fixed rate now, you will be ahead in most scenarios.

After the anticipated September 29 RBA rate hike, acting now will have saved you even more.

The above tables are general. You need to run these options using your own current home loan situation. And that is easy to do using our interactive mortgage table page.

Being active now will save you real money on your household budget. Otherwise those rising mortgage payments will end up in your bank's bottom line.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.