Term deposit rates of 5% or higher are now ubiquitous for terms of one year or longer.

In fact at some banks, these rates are as high as 5.35%.

But 5% rates are also shifting into less-than-1 year term deposit offers.

ANZ now offers 5% for just five months.

And for just four months Heritage Bank offers 4.85%, with AMP and Suncorp at 4.75%.

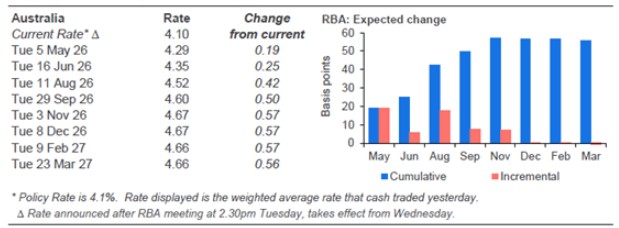

With wholesale markets pricing in a +25 bps RBA rate hike at their June 16 review, and another +25 bps by their September 29 review, the whole rate set is likely to rise for most of 2026.

So that raises the question of whether you are better off grabbing the widely available 5.20% to 5.35% one year rates now, essentially locking in those rates until May 2027, of take a 4.85% four month rate now so that by September you get one year rates that may have risen +50 bps by that time.

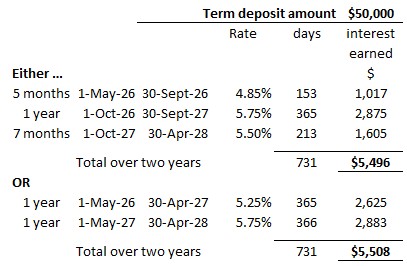

The math is clear. These rates are set so that there is essentially no difference between the two options if things play out as wholesale markets currently suggest. Here is the money based on a $50,000 term deposit. It will be exactly the same for any amounts $10,000 to $1 mln on a relative basis.

You are on your own judging what the future will bring. Based on what we know now, there is little difference, so your decisions center around how likely future rates will behave as the professionals are suggesting. Professional judgements are often wrong (although not always), and your gut feeling probably is just as reliable. Start by assessing whether you agree with the professionals that there will be only two +25 bps RBA rate hikes over the next two years.

And that depends on your view on how well inflation will be contained and whether RBA monetary policy actions will be effective. If you think the RBA has a generally good handle on things, the above scenario remains valid. If you think inflation will rise, then future rates are likely to be higher, so the first option will tend to give better results. If you think inflation will revert lower, more quickly that currently expected, the second option will be preferred.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.