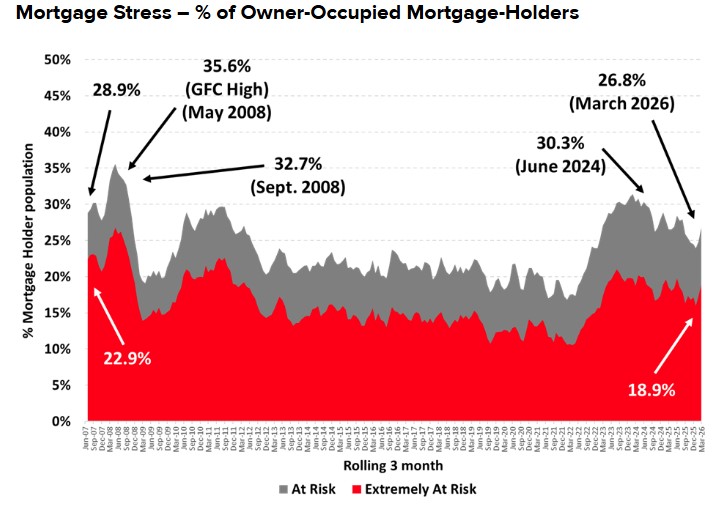

New research from Roy Morgan shows 26.8% of mortgage holders ‘At Risk’ of ‘mortgage stress’ in the three months to March 2026, up 1.9% points from February 2026, after the Reserve Bank raised interest rates for a second straight month in March by +0.25% to 4.1%.

A share of 26.8% of mortgage holders ‘At Risk’ of mortgage stress is equivalent to 1,447,000 people – up 130,000 on a month ago. The record high of 35.6% of mortgage holders ‘At Risk’ of mortgage stress was reached back in mid-2008.

The number ‘At Risk’ of mortgage stress is virtually unchanged on a year ago

The number of Australians ‘At Risk’ of mortgage stress is virtually unchanged on a year ago after the Reserve Bank cut interest rates in May 2025 (-0.25%) and August 2025 (-0.25%) but then raised them back up in February 2026 (+0.25%) and last month in March 2026 (+0.25%). As a result of these changes, interest rates at 4.1% are identical to a year ago.

The number of Australians considered ‘Extremely At Risk’, is now numbered at 1,020,000 (18.9% of mortgage holders) which is significantly above the long-term average over the last two decades of 16.3%.

Source: Roy Morgan Single Source (Australia), average interviews per 3 month period April 2007 – Mar 2026, n=2,889. Base: Australians 14+ with owner occupied home loan.

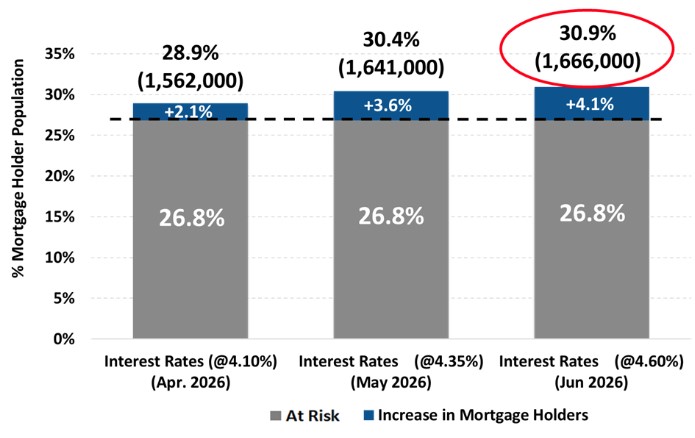

Mortgages ‘At Risk’ is set to rise if the Reserve Bank increases interest rates in May and June

The Reserve Bank raised interest rates in February and March by a total of 0.5% to 4.1%. These increases were due to a doubling in the official ABS annual inflation which hit a low of 1.9% in the year to June 2025, and has since almost doubled – the latest figure is 3.7% in the year to February 2026.

Because of this, Roy Morgan modelled the impact of potential RBA interest rate increases at its May 2026 meeting (+0.25% to 4.35%) and another potential interest rate increase in June 2026 (+0.25% to 4.6%).

In March, 26.8% of mortgage holders (1,447,000) were considered ‘At Risk’. Following the RBA’s decision to increase interest rates in March the share ‘At Risk’ is set to increase to an estimated 28.9% (up 2.1% points from March) in April and equivalent to 1,562,000 mortgage holders (up 115,000).

If the RBA raises rates in May by +0.25% to 4.35%, the share of mortgage holders ‘At Risk’ is forecast to rise to 30.4% (up 3.6% points from now) and equivalent to 1,641,000 mortgage holders, up 194,000 from now.

If the RBA raises rates in June by 0.25% to 4.6% the share of mortgage holders ‘At Risk’ would increase to 30.9% – up 4.1% points from now and equivalent to 1,666,000 mortgage holders, up 219,000 from now.

Mortgage Risk projections based on interest rate increases in May and June 2026 by 0.25% each

Source: Roy Morgan Single Source (Australia), January 2026 – March 2026, n=3,457. Base: Australians 14+ with owner occupied home loan.

How are mortgage holders considered ‘At Risk’ or ‘Extremely At Risk’ determined?

Roy Morgan considers the risk of ‘mortgage stress’ among mortgage holders in two ways:

Mortgage holders are considered ‘At Risk’ [1] if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending.

Mortgage holders are considered ‘Extremely at Risk’ [2] if even the ‘interest only’ is over a certain proportion of household income.

Unemployment is the key factor which has the largest impact on income and mortgage stress

It is worth understanding that Roy Morgan uses a conservative forecasting model, essentially assuming all other factors apart from interest rates remain the same.

The latest Roy Morgan unemployment estimates show over one-in-five Australian workers are either unemployed or under-employed – 3,380,000 (20.9% of the workforce); (In March, overall Australian unemployment and under-employment was at 3.38 million, ‘Real unemployment’ at 1.69 million).

Although the Reserve Bank’s decision to cut interest rates three times last year had a positive impact and helped lower mortgage stress, since the turn of the year the Reserve Bank has reversed course and has now increased interest rates on two occasions already this year.

Despite the actions of the Reserve Bank, the fact remains the greatest impact on an individual, or household’s, ability to pay the mortgage is not interest rates, it’s if they lose their job or main source of income. In addition, the intense economic uncertainty provided by the renewed conflict in the Middle East is already pushing energy prices higher and will add further pressure to inflation in the months ahead.

This is a re-post of the original here.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.