This year’s budget, with its focus on intergenerational distribution, will have significant effects on property and other asset markets, as well as on how many families manage their affairs. Even once they move beyond a pure winners-versus-losers framing, though, proponents of the changes and detractors alike are mostly thinking about fiscal policy like microeconomists. The emphasis is on efficiency and incentives across different activities and asset classes. Only rarely are macroeconomic perspectives, like the role of the fiscal system in managing the economic cycle, the focus.

The micro perspective stems from a deep-seated belief that fiscal policy cannot be used effectively to manage the macroeconomic cycle. Even though payments and other fiscal actions can affect demand immediately, the decision-making process is too slow, and prone to being politicised. And with many moving parts, a budget can be directed to other objectives. Best leave the macro side to monetary policy, goes the thinking. It has much faster decision-making cycles, and you can dedicate one instrument to one job.

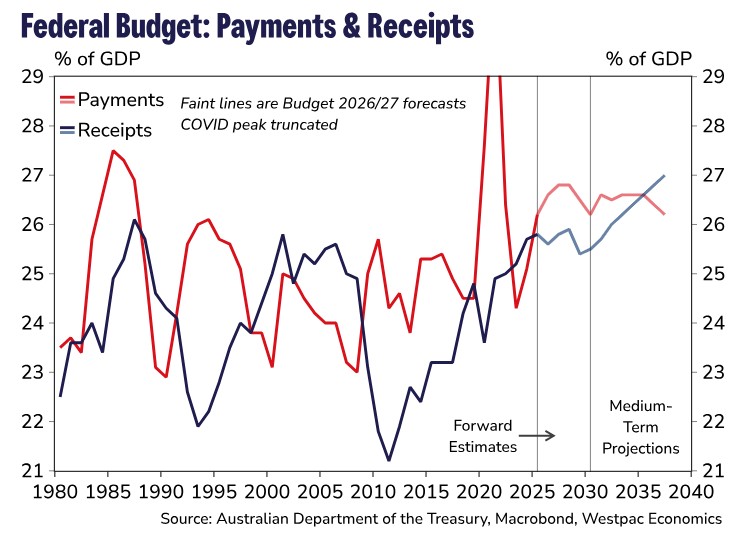

Even if you take this allocation of responsibilities as given, though, there is plenty that fiscal policy can learn from monetary policy. One example is evident in the medium-term projections beyond the four-year ‘forward estimates’ horizon of the budget. These projections show a comforting upward trend in tax revenue as a share of GDP that closes the current deficit out in the 2030s. This is because the projections take current policy as given – including the tax brackets, which are fixed in dollar terms. There are some revenue measures as well, including the tax changes announced in last week’s federal budget, but it is mostly bracket creep.

The reality is that, by the time we get to the 2030s, future governments will have given some of that bracket creep back. They always do. The alternative is an ever-rising share of household income going to tax. This inconsistency between forecasts based on known policy and the outcomes that are likely to actually occur once we get there is analogous to the ‘time-inconsistency problem’ that is well known to analysts of monetary policy.

The ‘inconsistency’ is that monetary policymakers will always be tempted to ‘cheat’ on an inflation target, choosing a bit more inflation in the near term to get a bit less unemployment. Without some suitable institutional constraints, a central bank therefore cannot credibly commit to keep future inflation at the desired rate. Resolving this inconsistency is one of the reasons why independence of the central bank is seen as so important.

So too with fiscal policy. A government can project to close a fiscal deficit using the increasing revenue from bracket creep. But when the day comes, the temptation to moderate an ever-increasing tax burden is too great. Just as central banks cannot credibly pre-commit to hit inflation targets without independence, accountability or some contractual arrangement, governments cannot credibly commit to improving their finances via future bracket creep. (To be clear, budget deficits of the order of 1% of GDP are not a big deal in the scheme of things, especially compared with most other major economies. But if your ostensible aim is to eliminate that deficit eventually, projections that assume full bracket creep are not credible indications that you will get there.)

Proposals to index tax brackets in some way can been seen in this context as a kind of pre-commitment device, much like independence and inflation targets are for monetary policy. Instead of giving periodic tax cuts but pretending you will not, bracket indexation legislates the unwind of bracket creep in a more mechanical way. It also avoids the risk that the usual decision and implementation lags end up seeing ad-hoc bracket adjustments arrive when the economy is hot and tax cuts are least needed.

Of course, medium-term projections formulated on this basis will look more alarming than the recent run of budget papers. The gap is more appearance than substance, however. Perhaps, though, this will bring forward the hard conversations about the appropriate size of government and the share of government spending in GDP. This share took a noticeable step up in the late 2010s and again since the pandemic. Bracket creep enabled this expansion in government payments without needing to raise taxes explicitly.

Plans to rein in NDIS spending should help avoid a further ramp-up in payments and the fiscal sustainability issues that would ensue. As we noted on Budget night, though, executing on these plans is crucial but far from assured.

This points to another lesson that fiscal policy can learn from monetary policy: that while a hard-and-fast policy rule is too rigid and too simplistic, there are benefits to some degree of automaticity, of counter-cyclicality by design. A progressive tax system like Australia’s embeds countercyclicality. When the economy is growing quickly, incomes rise. More of people’s income is then taxed at their top marginal rate and more people get pushed into higher tax brackets. This raises the share of income going to tax. As long as the revenue windfall is not automatically recycled as higher government spending, this effect dampens demand automatically. Targeted welfare systems help on this front, too. For the record, Australia’s system is widely regarded as more targeted than most developed countries’ systems.

Indexation of tax brackets, like periodic tax cuts, reduces the drag from bracket creep but can lose that countercyclical feature depending on how it is implemented. For this reason, we have previously argued that fixed indexation at 2.5% – the mid-point of the RBA’s inflation target – is in most cases preferable to CPI indexation. (This point also applies to calculation of capital gains tax, administered prices and some payments as well as income tax brackets.) That way, when the economy is strong and inflation is high, the tax system still leans against inflation somewhat. The central bank does not have to shoulder the burden of macroeconomic management alone.

The political nature of fiscal policy means there will always be some level of ‘consistency problem’. But careful design, including automation of some settings, can help address this. That in turn means fiscal policy can be more usefully used as a macroeconomic management tool, without risking the credibility of its medium-term sustainability.

Luci Ellis is the Group Chief Economist at Westpac. The original is here.

Comments

We welcome your comments below. If you are not already registered, please to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments.

Please to post comments.